Adapt or Die? A Deep Dive into SIA's Top Megatrend of 2025

This article originally appeared as the cover story in the January 2025 issue of Security Business magazine. Don’t forget to mention Security Business magazine on LinkedIn and @SecBusinessMag on Twitter if you share it.

Fast-forward just 12 months, and those AI-based megatrends and others have created a perfect storm of technology converging to impact integrators more fully and more quickly than they ever imagined possible. Together, the cloud and AI are making the not-so-simple task of integration much easier, and that same technology confluence is making it easier for new players – from manufacturers to distributors to IT service providers – to deliver remote diagnostics, support, repair, and maintenance to physical security products.

As these technology solutions evolve faster than ever, integrators are struggling to stay informed, trained, and up to date. Margins are tightening even more than they already were, and new challengers to the integrator’s decades-established role are emerging.

Meanwhile, as more private equity firms enter the security integration industry, they are demanding the acquired integrators deliver more RMR utilizing newer security industry as-a-service business models to justify what is often a very sizeable investment.

The result is SIA’s top 2025 Security Megatrend: The evolution of the channel.

“In last year’s report, AI earned the top four spots, and it really was a watershed moment for our industry,” explains Geoff Kohl, SIA’s Senior Director of Marketing , who authors the annual report based on the insights of a group of advisors plus feedback from focus groups and an annual survey of SIA members. “This year’s top megatrend is the evolution of the channel. It was just very clear that more than the technology change of AI, people were concerned about the changes that are happening within the channel – particularly within the systems integrator world, but also within distribution.”

The SIA Megatrends advisors included: Former PSA Security CEO Bill Bozeman, Wesco’s Tara Dunning, consultant Kasia Hanson, Allegion’s Devin Love, John Mack of Imperial Capital, Faisal Pandit of Johnson Controls, Brian Ruttenbur of Alarm.com, Brivo’s Steve van Till, and Eric Yunag of Convergint.

To discuss the evolution of the channel, we caught up with Yunag and Bozeman.

Technology Modernization

According to Yunag, the macro trend that is most affecting the channel is a confluence of technology modernization trends. This not only includes AI and cloud, but also IoT architectures, enterprise software, data convergence, and more.

“You have to put all of those things together when you think about the evolution of the channel,” Yunag says. “It is really important to look at the technology in totality, but my personal opinion is that it doesn't change much for the integrator – in the sense that there will always be devices in the field that have to be managed, whether the application sits on-premise or it sits in the cloud. What has changed is the delivery of the software that manages those devices and ultimately delivers the outcomes and limits risks for end-users. The thing that changes relative to the channel and the way things are delivered, ultimately, is the collaboration required between application developers, end-users, and integrators.”

The software delivery aspect is what has changed so drastically for commercial integrators. Things are very different than years past when a typical security end-user aimed to upgrade premise-based physical access control systems once a year and their dependency on physical hardware was relatively straightforward.

“When there are new upgrades to cloud applications that bring new features or new capabilities in rapid succession many times throughout a year – whether for access control hardware or cameras or other things – all of that has to be orchestrated and managed in a way that delivers the outcome the end-user needs,” Yunag explains. “The complexity gets higher, even though the speed of innovation is driving new abilities to solve problems and limit risk. From the integrator’s perspective, we remain central to the orchestration of all that.”

Emerging Competition for Technology Delivery

Dating back to his days running an integration company himself and later advising integration company owners as CEO of PSA, Bozeman has long been a proponent of evolving the channel. He was one of the first to bang the drum about creating recurring revenue, and that evolved into advising companies to literally become managed service providers.

“Bill has talked about this for a decade or better,” says Yunag, who was one of those PSA owners when he ran his own integration company, Dakota Security Systems, before being acquired by Convergint in 2016. “Between recurring revenue and services for integrators, the technology modernization, and the changing dynamics of end-user risks, when you smash all that together, you can really see the overlap. Those traditional swim lanes of all the different players bringing solutions to market are really starting to blur.”

Bozeman is quick to counter that the days of an integrator simply relying on project-based revenue aren’t necessarily over, but it will require a change in perspective.

“Some integrators will benefit a lot, but others will get crushed,” he says. “Others will simply become deploying agents similar to an electrical contractor. You can make a good living as an electrical contractor – it is just a different type of business. The integrator is behind the eight-ball in a lot of cases, simply because most of them don’t have much of a recurring revenue model at a higher gross margin than their traditional install business. A traditional install business is a low-margin business. It just is.”

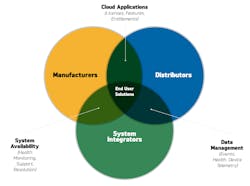

At Securing New Ground in October, Yunag spoke on a panel focusing on the Megatrends, and he unveiled a Venn diagram that crystallizes his thoughts on how the delivery model for the channel is changing. It illustrates the growing competition over the customer – in this case, the security end-user.

This creates the emergence of overlapping services that the manufacturers, distributors, and integrators are all vying to deliver: cloud applications, system monitoring, and data management.

“There is 50 years worth of muscle memory in this industry of integrators doing projects and being construction contractors,” Yunag says. “It is the way this channel works – that linear flow chart of the manufacturer to the distributor to the integrator. The move to services is the center of the diagram and is creating overlap between all those partners. That’s why the channel is confusing now – because all of the partners are moving to services.”

This is where we are seeing new players emerging with new business models. Manufacturers like Flock and Axon, for example, are marketing plug-and-play solutions directly to the end-user – cutting channel players like integrators and distributors out of the equation entirely in many cases. Verkada notoriously came to market with this model but has now somewhat embraced the channel with various integrator partnerships.

“I have been an integrator my entire life, and I always had a visceral, bristling response to product manufacturers having conversations with end-users that were ‘my customers,’” Yunag says. “The pace of technology change is so different today, and now I have a better appreciation or understanding of the evangelism that has to take place on new technologies, new models, and a new way of delivering security outcomes. I have come to separate companies trying to tell their story and how they get implemented, delivered, and maintained in the end.”

That said, end-users are noticing these new interactions. “One of the great points that Eric made at Securing New Ground was highlighting the interaction between manufacturers and end-user practitioners, or even between the distributor and the practitioner,” Kohl notes. “That interaction is what they remember rather than the relationship that they have with the integrator. I think that’s what’s changing.”

After listening to a panel of enterprise security directors at Securing New Ground, Bozeman was struck by their dissatisfaction with the channel. “They basically came out and said, ‘If you guys don’t clean your act up, we’ll just do it ourselves,’” Bozeman notes.

“For an end-user, it becomes more difficult to hold people accountable and to get a total solution delivered,” Yunag adds. “Just reading back on my notes on that Securing New Ground session, those end-users were asking their integrators for turnkey solution delivery. They asked us to listen. They asked us for DRIs – directly responsible individuals – for the whole technology stack. When I hear those things, I hear them telling us they want to have somebody accountable and capable of executing on delivering solutions that ultimately solve their problems.”

One Result: More Channel M&A

Enterprise integrators faced with this evolving challenge are often confronted with the classic choice: Fight or flight. That means many have embraced this change and are evolving; others are choosing the second option.

“Some smaller integrators are realizing that it might be a good time to sell because the prospect of keeping up with the Convergints and JCIs of the world is daunting,” Bozeman says.

Security company acquisitions are bearing that out. As written in these pages frequently over the past 24 months, private equity-backed conglomerates and major security players are all in fierce competition for the acquisition of mid-level and super-regional security integrators.

“Simply put, there are not many integration companies in this industry bigger than $50 or $100 million,” Yunag says. “Convergint didn’t get this big by acquiring huge integrators – the $10-$40 million integrators are the sweet spot.”

That said, from the private equity perspective, Bozeman says PE attention has shifted to the fire side of the business. “Right now, they are looking more at fire and life safety than they are at physical security systems integrators,” he says.

Where do Integrators go from Here?

Those integrators who embrace the fight response and want to adapt and thrive in the new definition of the channel need to face certain truths – a primary one being to focus on the enterprise space. As Yunag puts it, “If you are not in a market where [security technology] is mission-critical, it is tough to provide value.”

!['My hardwired true north is always to listen to what the customer is telling me, and what I hear from customers every day is that they want [integrators] to take more ownership of the security outcomes that they are delivering,' Yunag says.](https://img.securityinfowatch.com/files/base/cygnus/siw/image/2024/12/6769be5a395146956c9b5c02-54071317871_0a04fed119_o.png?auto=format,compress&fit=max&q=45?w=250&width=250)

Importantly, adapting to the new channel environment means doing what those enterprise end-users were asking: To listen.

“My hardwired true north is always to listen to what the customer is telling me, and what I hear from customers every day is that they want [integrators] to take more ownership of the security outcomes that they are delivering,” Yunag says. “You need to understand their organizational requirements – the real things that are driving decision-making – and then design and put together the systems, structures, software, and hardware programs –including the purchasing, installing, and the project management – to do that. If you do those things well, people will pay you for them. If you are ‘just good at installing,’ then there is a good chance you will get outbid in very commoditized ways.”

Yunag adds that the program and project management for complex global rollouts is a discipline and skillset all its own, and those services are well monetized and margined because they deliver a high amount of value to customers. That also presents an opportunity to engage with new manufacturers, and software and cloud providers – all with the goal of helping customers solve problems in more dynamic ways that they couldn’t do previously.

“That entire lifecycle is full of opportunities for this industry – integrators particularly – to deliver value to customers around a service delivery model that helps customers streamline and accelerate security outcomes and limit risks,” Yunag says. “Integrators can’t do that unilaterally – it requires collaboration, orchestration of a bigger and bigger ecosystem of more and more moving parts. But if you do that well, you’re going to get paid for it, whether you are an integrator worth $10 million or a billion. That’s me on the soap box, but I think that is where our industry is going.”

To read the full SIA Megatrends report, visit https://www.securityindustry.org/report/security-megatrends-the-2025-vision-for-the-security-industry/

About the Author

Paul Rothman

Editor-in-Chief/Security Business

Paul Rothman is Editor-in-Chief of Security Business magazine (www.securitybusinessmag.com) and has been covering the security industry for various outlets since 2001. Email him your comments and questions at [email protected].